Nearly 9 in 10 people say accurate, on-time pay makes them feel respected by their employer. That respect shows up in practical outcomes like the correct tax code on their first payslip, accurate statutory deductions, and pay that runs without post-payday corrections.

Nothing shapes a new joiner’s experience quite like a smooth onboarding process, especially one where finance sets up their pay correctly and it arrives exactly when it should.

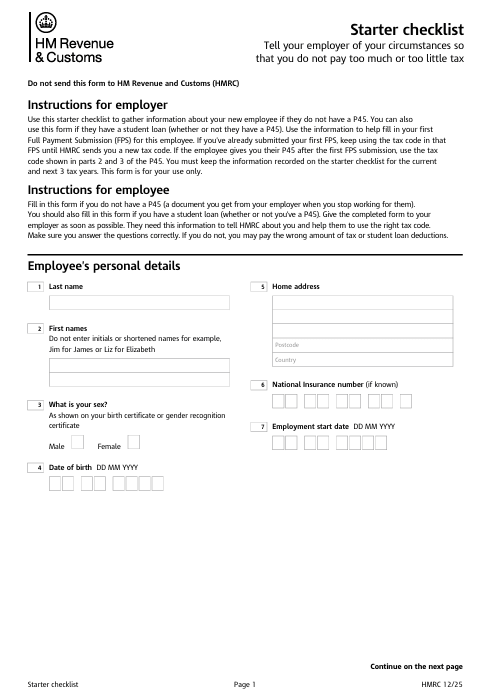

For new joiners in the United Kingdom, His Majesty’s Revenue & Customs (HMRC) new starter checklist is behind how payroll comes together during onboarding. The form gives employers a reliable way to meet their tax obligations while keeping onboarding compliant and consistent.

This guide explains what the HMRC new starter checklist is, when it’s required, and how to use it to support a reliable UK payroll experience for every new joiner.

Key insights

- The HMRC new starter checklist helps employers collect tax information from new joiners in the UK

- It supports accurate tax code setup, smoother first pay runs, and fewer follow-up payroll changes

- The checklist applies when a team member doesn’t have a valid P45, is working in the UK temporarily, or has a student or postgraduate loan to declare

- Teams typically include the checklist during preboarding, alongside other payroll details, to have everything ready before the first pay run

- Common mistakes that affect first pay runs include collecting the checklist too late, using it when a valid P45 is available, or choosing the wrong starter statement

- Storing completed checklists in a shared HR or payroll system helps teams work from consistent information

What is the HMRC new starter checklist?

The HMRC new starter checklist is a form new joiners fill out when they start a job in the UK. “It helps employers operate the correct tax code against a team member’s income, and minimizes the risk of under or overpayments,” says Suzanne Goodier-Dodson, Payroll Manager at The Accountability Partnership. Employers use the information to add the new joiner to their payroll software and notify HMRC ahead of their first payment.

Who fills out the new starter checklist?

New joiners complete the starter checklist themselves, using either HMRC’s official form or as part of their employer’s essential onboarding documents. “The checklist is between an employer and team member and isn’t sent to HMRC,” says Suzanne Goodier-Dodson. Instead, payroll sends the relevant details to HMRC on the new joiner’s behalf to issue or confirm their tax code.

When do you need a new starter checklist?

A new starter checklist applies when a team member:

- Doesn’t have a P45 (a form issued by an employer when a team member leaves a job, showing their pay and tax paid to date)

- Has a P45 with incorrect or outdated personal details

- Is working in the UK temporarily for an overseas employer

- Has a student or postgraduate loan to declare

Is the new starter checklist the same as a P46 form?

The new starter checklist is the digital-friendly replacement for the P46 form, which HMRC officially withdrew in 2013. With the old P46 process, you had to print the form, fill it in by hand, and mail it to HMRC for a tax code. In contrast, the HMRC starter checklist fits naturally into modern payroll workflows. You complete it online, keep it on record, and submit it through Real Time Information (RTI) with the first pay run.

Why is the new starter checklist important?

The new starter checklist plays a central role in how onboarding and payroll come together for new joiners and payroll teams alike. It touches everything from tax setup and compliance to onboarding flow and first impressions. Here’s how.

Recommended For Further Reading

- Payroll year-end checklists for UK businesses in 2025

- Global payroll systems: Building your multi-national strategy

- The payroll metrics that matter most

- BACS vs Faster Payments

- What is payroll automation?

- Weekly payroll: How it works and top benefits

- Simplify UK payroll with end-to-end HR and payroll software

Tax code accuracy

“HMRC uses [the checklist] data from the first RTI submission to match the new joiner to existing records,” says Peter Bickley, Technical Manager of Employment Taxes at the Institute of Chartered Accountants in England and Wales. This is to review the tax code applied in payroll and confirm whether it aligns with the new joiner’s tax position for the year to date.

If HMRC determines that a different tax code applies, it issues the updated tax code to the employer and payroll applies it to subsequent pay runs. That way, tax deductions reflect the team member’s overall position for the tax year accurately and reduce the likelihood of follow-up corrections.

PAYE compliance

From a compliance perspective, the HMRC new starter checklist supports accurate Pay As You Earn (PAYE) reporting through RTI. When a new joiner doesn’t have a valid P45, it becomes the mechanism employers use to add them to HMRC’s system and report their starter details correctly in the first Full Payment Submission (FPS). This helps payroll stay aligned with HMRC reporting requirements from the start.

Onboarding efficiency

Onboarding involves many moving parts, from contracts to employee benefits. Because the checklist captures all the information needed for payroll setup in one place, it supports smoother handoffs between teams and reduces the need for follow-up questions once payroll processing begins.

Team member satisfaction

An error-free first payslip helps build trust early on, especially since 90 percent of people say it’s important for employers to support financial wellness. “Payroll is an emotional process,” says Dr. Sven Elbert, Lead HCM Analyst at Fosway Group. “People rely on being paid correctly and on time to live their lives.”

The new starter checklist supports that experience by helping payroll get set up correctly before the first pay run—and giving new joiners the financial peace of mind they deserve.

How to help team members complete the HMRC new starter checklist

New joiners might need help with certain parts of the starter checklist process, including:

1. Accessing the checklist

Share the HMRC new starter checklist with team members as part of your onboarding process, either through HMRC’s website or your payroll software provider. Include a short note that covers:

- What the checklist affects: Tax code setup and student loan deductions

- Who needs to complete it: New joiners without a P45 or with changes to declare

- What happens after submission: Details flow into payroll with no direct confirmation from HMRC

This approach helps new joiners understand the process and minimizes first-day overload.

2. Adding personal details

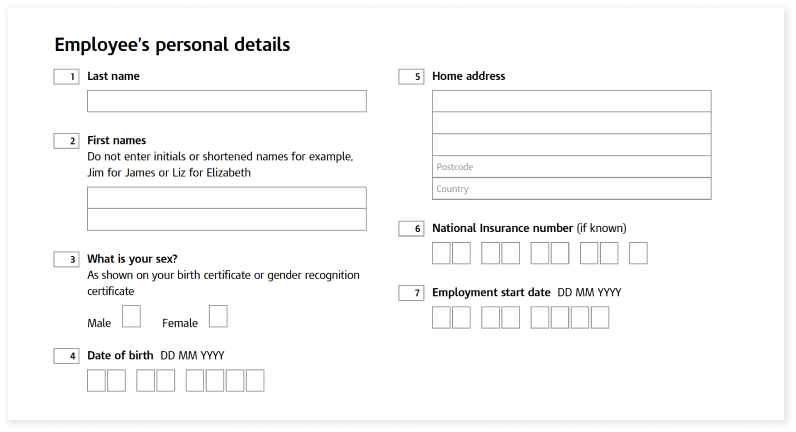

Since you can’t save the HMRC new starter checklist and return to it later, it’s worth letting new joiners know what to have ready before they start. The form asks for the following personal details:

- Full name, address, and date of birth

- Start date

- National insurance number

- Student loan or postgraduate loan status

- Previous tax code information (if available)

- Other income earned in the current tax year (from sources like a jobseeker’s allowance, pension, or incapacity benefit)

- Passport number (if they’re working in the UK temporarily)

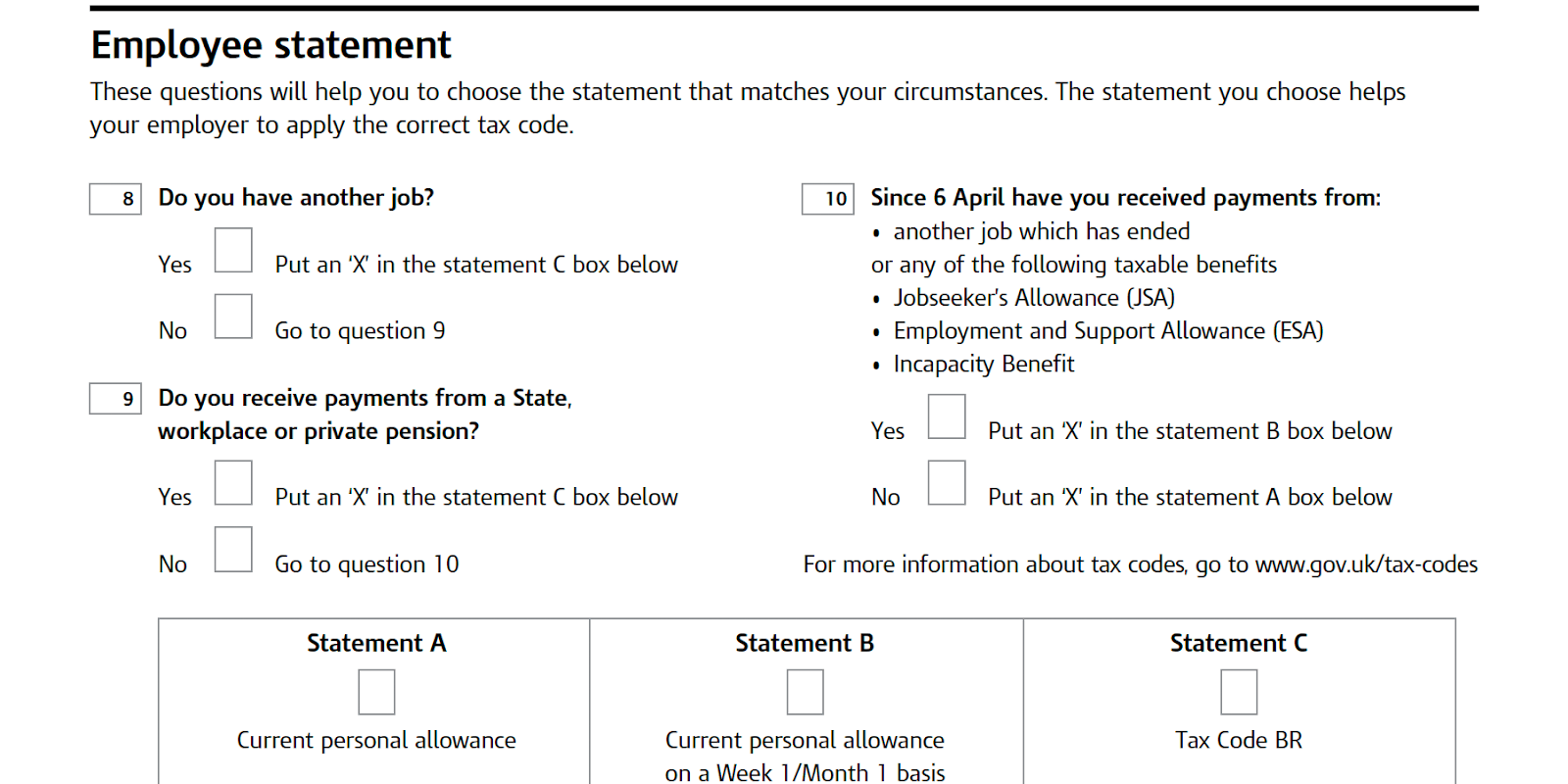

3. Selecting the right employee statement

The checklist asks new joiners whether they have another job or receive a state, company, or private pension, then prompts them to choose a statement that best reflects their situation. Each statement links to a different tax setup, which impacts the tax code assigned and the taxes they pay:

Statement A

Statement A applies to new team members working their first job since April 6 of the current tax year who haven’t received a taxable state pension, occupational pension, incapacity benefit, jobseeker’s allowance, or employment and support allowance.

Statement B

Statement B applies to team members who work only for your business but have had another job since April 6 of the current tax year and don’t have a P45. It also applies if they’ve received a taxable incapacity benefit, employment and support allowance, or jobseeker’s allowance in the current tax year.

Statement C

Statement C applies to team members who have another job and/or have received a taxable private state or works pension in the current tax year.

New joiners often pause at this step if they’ve changed jobs, held more than one role since April, or receive a pension, since the statement reflects tax already applied in the current tax year. Confirm whether they’ve received pay from another employer since April 6 to confirm which statement applies and how HMRC will set the tax code.

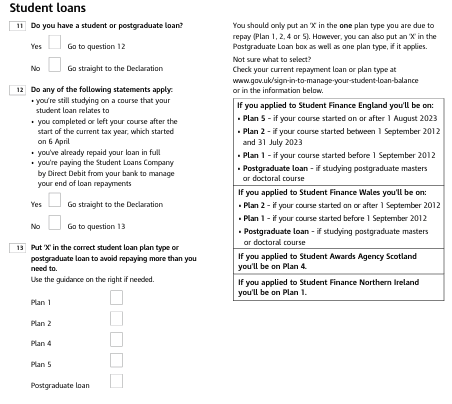

4. Completing the student loan declaration

Student and postgraduate loan details affect whether payroll applies deductions, but new joiners might not know their loan plan type or if repayments are still active. Ask them to check their most recent payslip or their HMRC account for the correct details before filling out this section.

How to accurately complete the HMRC new starter checklist as an employer

Once a new joiner hands in their filled checklist, HR teams finish the process. They will:

1. Determine the NIC category

Set your new team member’s National Insurance Contribution (NIC) category first thing, using their age, earnings, and circumstances as your guide. Payroll systems tend to apply default categories from templates or prior records, so early confirmation helps keep calculations aligned.

2. Submit the new starter checklist to HMRC

Once you finalize the checklist, enter the starter details into your payroll system. This adds your new joiner’s information to the next FPS, giving HMRC time to issue a tax code ahead of their first payday.

Common mistakes to avoid when filling out the HMRC new starter checklist

Small oversights during the starter checklist process can impact tax codes and payroll timing. To keep first pay runs accurate and onboarding on track, check for common payroll challenges and mistakes, such as:

- Collecting the checklist too late: Late collection can leave payroll without the information needed to apply the correct tax code. Request the checklist as part of your preboarding paperwork so payroll receives the details before the first pay run.

- Using a checklist when a valid P45 exists: Submitting both documents can create conflicting tax records with HMRC. Ask new joiners whether they have a P45 and use it instead of a checklist when available.

- Letting new joiners choose a statement without guidance: Starter statements depend on employment history and current circumstances. Explain what each statement means and confirm the correct option with your new joiner.

- Assuming HMRC will automatically correct errors: Tax code updates may not align with payroll timelines. Review your new joiner’s first payslip as a precaution and address any tax code issues right away.

- Submitting the checklist without a final review: Small data errors can delay processing or trigger manual corrections later. Check key fields like National insurance number, date of birth, and student loan plan type before submission.

- Using the checklist for returning team members: Boomerang employees don’t always follow the same tax process as new joiners. Confirm whether they qualify as a new starter before completing a checklist.

- Reusing older checklist templates: HMRC updates forms and guidance periodically. Download the current checklist directly from HMRC instead of using stored copies.

- Storing completed checklists inconsistently: Checklist data stored across separate tools leads teams to work from different versions of the same information. Use HR software to organize starter documents in one central place for all teams.

Streamline the new starter checklist process for your team

Streamlining your company’s HMRC new starter checklist process supports a smoother onboarding experience for your team. It enables them to manage and apply tax codes accurately, avoid unnecessary delays and penalties, and help new joiners feel welcomed and prepared from day one.

And if HR compliance questions come up along the way, you can always refer to the official HMRC new starter guidelines to stay aligned with current requirements.

New starter checklist FAQ

What is a new starter checklist for?

Companies use the HMRC new starter checklist to collect information from new joiners in the UK so they can set them up on payroll. It helps you apply the right tax code to your people’s earnings and minimize the risk of under or overpaying tax.

Does a P45 replace the starter checklist?

Not always. You can use a P45—the form a previous employer gives someone showing their pay and tax details—when onboarding a new starter as long as it’s available and still applies. But if a new joiner doesn’t have a P45, or the details are no longer relevant (for example, after a long break from work), you use the starter checklist instead (formerly the P46).

Is HMRC’s starter checklist a P46?

No, the HMRC new starter checklist isn’t a P46—but it does serve as its replacement. The starter checklist is now the official form to determine a new joiner’s tax code, even though many people still refer to it by the old name.

Does a new starter checklist prevent an emergency tax code application?

No, a new starter checklist doesn’t prevent the application of an emergency tax rate. In certain situations, even if someone has completed a starter checklist, an employer may apply an emergency tax code to their salary.

For example, HMRC doesn’t always deliver a new joiner’s tax information before their first day. If that happens, you apply an emergency tax code until HMRC sends you the correct one.

What does an employer do without a new starter checklist?

In the absence of a starter checklist or a P45, place new joiners on starter declaration code C and use tax code 0T.

Is the HMRC new starter checklist mandatory?

HMRC doesn’t describe the starter checklist as mandatory explicitly, but it’s considered the standard way to set up new joiners on payroll and report details through RTI. It lets you set the correct tax code from day one instead of applying an emergency code and correcting payroll later.